Affordable Healthcare for Gig Workers: Maximizing 2026 Tax Credits for Health Insurance Premiums

In the rapidly evolving landscape of the gig economy, the promise of flexibility and autonomy often comes with a significant challenge: securing affordable healthcare. Unlike traditional full-time employees who typically receive employer-sponsored health benefits, gig workers are largely responsible for their own health insurance. This responsibility can be a daunting financial burden, leading many to forgo essential coverage, risking both their health and financial stability. However, with the continued support of government initiatives, particularly the enhanced tax credits available through the Affordable Care Act (ACA), there’s a beacon of hope for Gig Worker Healthcare 2026. Understanding and maximizing these tax credits is not just about saving money; it’s about securing peace of mind and ensuring access to vital medical services.

The year 2026 is particularly significant as the enhanced subsidies from the American Rescue Plan Act (ARPA) are expected to continue, offering substantial financial relief to millions. For gig workers, who often experience fluctuating incomes and a lack of traditional employer benefits, these tax credits are a lifeline. This comprehensive guide will delve deep into the intricacies of these premium tax credits, providing actionable strategies for gig workers to navigate the health insurance marketplace, understand eligibility requirements, and ultimately reduce their healthcare costs. We will explore how to estimate income accurately, choose the right plan, and reconcile tax credits at the end of the year, ensuring you are fully prepared to capitalize on every available saving opportunity for Gig Worker Healthcare 2026.

The Gig Economy and Healthcare: A Growing Challenge

The gig economy has transformed the way many people work, offering unprecedented flexibility. From freelance writers and designers to ride-share drivers and delivery personnel, millions of Americans are now part of this dynamic workforce. While the allure of being your own boss is strong, the absence of a safety net, particularly regarding health insurance, is a major concern. Traditional employment models often absorb a significant portion of health insurance premiums, making comprehensive coverage more accessible. Gig workers, however, bear the full brunt of these costs, which can be substantial.

The financial strain of high premiums can lead to difficult choices. Many gig workers opt for high-deductible plans, or worse, go without insurance altogether, hoping they won’t face a medical emergency. This approach is fraught with risk. A single unexpected illness or injury can lead to crippling medical debt, undermining the financial independence that the gig economy promises. This vulnerability underscores the critical need for gig workers to understand and utilize all available resources to make healthcare affordable.

Beyond the financial aspect, the lack of consistent healthcare can have long-term health consequences. Regular check-ups, preventative care, and early treatment of conditions are often delayed or skipped, leading to more severe health issues down the line. This not only impacts individual well-being but also places a greater burden on the healthcare system as a whole. Therefore, empowering gig workers with the knowledge to access affordable health insurance is not just a personal benefit but a societal imperative, especially concerning Gig Worker Healthcare 2026.

Understanding the Affordable Care Act (ACA) and Premium Tax Credits

The Affordable Care Act (ACA), often referred to as Obamacare, was designed to make health insurance accessible and affordable for more Americans, including those who are self-employed or work in the gig economy. A cornerstone of the ACA is the Premium Tax Credit (PTC), a refundable tax credit that helps eligible individuals and families pay for health insurance purchased through the Health Insurance Marketplace. These credits can be taken in advance to lower monthly premium payments, or claimed when filing taxes.

The amount of the premium tax credit is based on a sliding scale, meaning that individuals and families with lower incomes receive larger credits. This makes health insurance more affordable for those who need it most. The ACA established specific income thresholds relative to the federal poverty level (FPL) to determine eligibility. Prior to the American Rescue Plan Act (ARPA), individuals with incomes above 400% FPL were generally not eligible for subsidies. However, ARPA significantly expanded eligibility and increased the generosity of these credits.

For Gig Worker Healthcare 2026, it’s crucial to understand that these enhanced subsidies are projected to continue. This means that individuals and families will pay no more than 8.5% of their household income for a benchmark silver plan, regardless of how high their income is. This ‘subsidy cliff’ was eliminated, making premium tax credits available to more middle-income households. This expansion is particularly beneficial for gig workers whose incomes might fluctuate or fall into income brackets that were previously ineligible for substantial assistance.

Eligibility for Premium Tax Credits in 2026

To qualify for premium tax credits in 2026, gig workers must meet several key criteria:

- Purchase Coverage Through the Marketplace: You must enroll in a health insurance plan through your state’s Health Insurance Marketplace (also known as the exchange or Healthcare.gov). Plans purchased directly from an insurance company outside the Marketplace are not eligible for tax credits.

- Income Requirements: Your household income must fall within specific guidelines. With the enhanced subsidies likely to continue in 2026, there is no income cap for eligibility. However, the amount of your credit will still be based on a sliding scale relative to the Federal Poverty Level (FPL). Generally, the lower your income, the higher your credit.

- Not Eligible for Other Coverage: You must not be eligible for other minimum essential coverage, such as Medicare, Medicaid, CHIP, or affordable employer-sponsored health coverage. If your spouse’s employer offers affordable coverage that meets minimum value standards, you might not be eligible for tax credits through the Marketplace.

- File a Joint Tax Return (if married): If you are married, you must file a joint tax return to be eligible for premium tax credits.

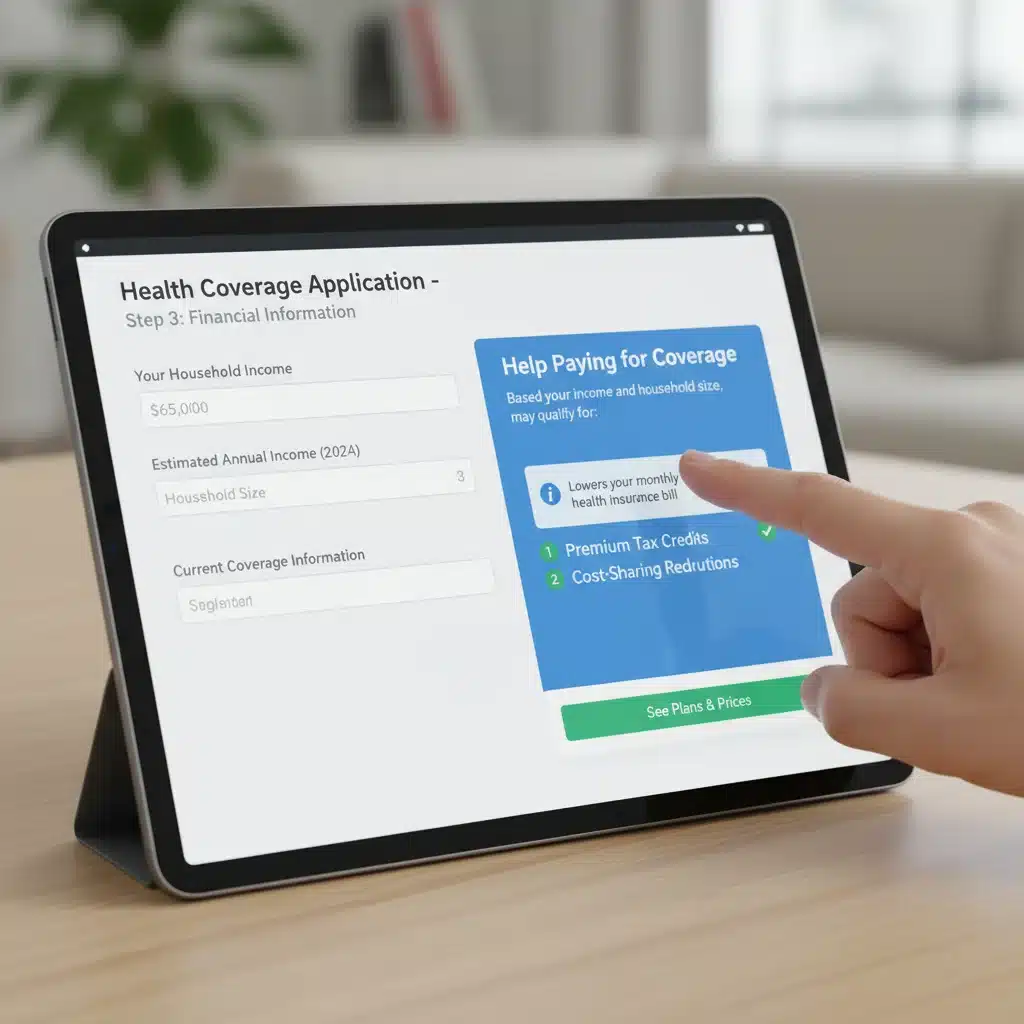

One of the biggest challenges for gig workers is accurately estimating their annual income. Since gig income can be irregular, it’s easy to under- or overestimate. However, an accurate estimate is vital because the amount of your advance premium tax credit (APTC) is based on this projection. Significant discrepancies between your estimated income and actual income can lead to adjustments when you file your taxes, potentially resulting in owing money back to the IRS or receiving a larger refund. We will delve deeper into income estimation strategies later in this guide for optimizing Gig Worker Healthcare 2026.

Maximizing Your 2026 Tax Credits: A Step-by-Step Guide

Navigating the health insurance marketplace and understanding tax credits can seem complex, but by following a structured approach, gig workers can effectively maximize their savings. Here’s a step-by-step guide:

Step 1: Accurate Income Estimation for Gig Workers

This is arguably the most critical step for gig workers. Your income directly impacts your eligibility and the amount of your premium tax credit. Given the fluctuating nature of gig work, this can be challenging. Here are some strategies:

- Review Past Income: Look at your income from the previous year, and the current year to date. This provides a baseline.

- Project Future Earnings: Consider your typical work patterns, anticipated projects, and any seasonal variations in your gig work. Be realistic but err on the side of caution.

- Account for Expenses: Remember that for tax credit purposes, your income is generally your Adjusted Gross Income (AGI). This means you can deduct legitimate business expenses associated with your gig work (e.g., mileage, supplies, home office deductions). These deductions can significantly lower your taxable income and increase your tax credit.

- Update Your Information: If your income changes significantly during the year (either up or down), it is crucial to update your information with the Marketplace immediately. This allows them to adjust your advance premium tax credits, preventing large reconciliation issues at tax time.

Underestimating your income could result in receiving too much in advance tax credits, which you would then have to pay back. Overestimating could mean you pay more for premiums than necessary throughout the year. The goal is to be as accurate as possible to optimize your Gig Worker Healthcare 2026.

Step 2: Navigating the Health Insurance Marketplace

Once you have a solid income estimate, it’s time to explore the Health Insurance Marketplace. This is the only place where you can access premium tax credits. Here’s what to do:

- Create an Account: Go to Healthcare.gov (or your state’s specific exchange website) and create an account.

- Provide Household Information: You’ll need to provide details about your household size, income, and any other sources of health coverage.

- Compare Plans: The Marketplace will present you with various plans categorized into metal tiers: Bronze, Silver, Gold, and Platinum.

- Bronze plans have the lowest monthly premiums but the highest deductibles and out-of-pocket costs. They are suitable for those who rarely visit the doctor.

- Silver plans offer moderate premiums and deductibles. They are particularly important because premium tax credits are based on the cost of a benchmark silver plan. Also, if your income is below a certain level, silver plans may offer additional “cost-sharing reductions” (CSRs) that lower your deductibles, copayments, and out-of-pocket maximums.

- Gold and Platinum plans have higher monthly premiums but lower deductibles and out-of-pocket costs, suitable for those who expect to use medical services frequently.

- Utilize the Plan Finder Tools: The Marketplace offers tools to compare plans side-by-side, considering premiums, deductibles, co-pays, and out-of-pocket maximums. Pay close attention to the network of doctors and hospitals to ensure your preferred providers are covered.

Step 3: Understanding Advance Premium Tax Credits (APTC)

When you apply for coverage through the Marketplace, you’ll have the option to have your estimated tax credit paid directly to your insurance company each month. This is known as an Advance Premium Tax Credit (APTC). By choosing this option, your monthly premium payments will be immediately reduced, making healthcare more affordable throughout the year. This is a critical feature for managing cash flow as a gig worker.

You can choose to take all, some, or none of your estimated tax credit in advance. While taking all of it upfront reduces your monthly burden, remember that it’s based on your estimated income. If your actual income ends up being significantly higher, you might owe some of the APTC back at tax time. Conversely, if your income is lower than estimated, you may receive an additional credit or refund.

Step 4: The Importance of Cost-Sharing Reductions (CSRs)

For gig workers with lower incomes, Silver plans offer an additional benefit called Cost-Sharing Reductions (CSRs). These are distinct from premium tax credits and reduce the amount you have to pay for deductibles, copayments, and coinsurance. CSRs effectively increase the actuarial value of a Silver plan, meaning the plan covers a higher percentage of your medical costs. You are only eligible for CSRs if you enroll in a Silver plan and your income falls within specific FPL thresholds (typically between 100% and 250% FPL).

If you qualify for CSRs, a Silver plan can often be a better value than a Gold or even Platinum plan, as it offers lower out-of-pocket costs at a more affordable premium. When comparing plans, the Marketplace will automatically show you if a Silver plan includes CSRs based on your income, making it easier to identify the best option for your Gig Worker Healthcare 2026 needs.

Reconciling Your Tax Credits: Form 8962

At the end of the year, when you file your federal income tax return, you will reconcile the advance premium tax credits you received with the actual premium tax credit you are entitled to based on your actual household income. This process is done using Form 8962, Premium Tax Credit (PTC).

The Marketplace will send you Form 1095-A, Health Insurance Marketplace Statement, which details the amount of advance payments of the premium tax credit that were paid on your behalf, as well as information about your monthly premiums. You will use the information from Form 1095-A to complete Form 8962. Here’s what can happen:

- You received too much APTC: If your actual income was higher than your estimated income, you might have received more APTC than you were eligible for. You will have to repay some or all of this excess APTC. However, there are repayment limits based on your income, which can shield lower-income individuals from having to repay the full amount.

- You received too little APTC: If your actual income was lower than your estimated income, you may be eligible for an additional premium tax credit. This will either reduce your tax liability or increase your tax refund.

- You didn’t take APTC: If you paid full price for your premiums throughout the year but were eligible for a premium tax credit, you can claim the entire credit when you file your taxes, which will either reduce your tax liability or result in a refund.

Keeping accurate records of your income and expenses throughout the year is crucial for a smooth reconciliation process. Regular review of your earnings and updating your Marketplace application if there are significant changes can help minimize surprises at tax time, ensuring you maximize your Gig Worker Healthcare 2026 benefits.

Additional Strategies for Affordable Gig Worker Healthcare

Beyond premium tax credits, gig workers can employ other strategies to make healthcare more affordable and accessible:

1. Health Savings Accounts (HSAs)

If you enroll in a High-Deductible Health Plan (HDHP) that is HSA-eligible, you can open a Health Savings Account. HSAs offer a triple tax advantage:

- Tax-deductible contributions: Money you contribute to an HSA is tax-deductible.

- Tax-free growth: The money in your HSA grows tax-free.

- Tax-free withdrawals: Withdrawals for qualified medical expenses are tax-free.

An HSA can be a powerful tool for gig workers to save for future medical expenses while reducing their taxable income. It provides a financial cushion for those high deductibles and acts as a long-term savings vehicle for healthcare costs, especially important for planning Gig Worker Healthcare 2026 and beyond.

2. Explore Medicaid and CHIP

If your income is very low, you might be eligible for Medicaid or the Children’s Health Insurance Program (CHIP). These programs provide free or low-cost health coverage. Eligibility rules vary by state, but if you qualify, these programs offer comprehensive benefits with minimal out-of-pocket costs. You can check your eligibility through the Health Insurance Marketplace application, which will automatically screen you for these programs.

3. Consider Professional Organizations and Associations

Some professional organizations, unions, or gig worker associations offer group health insurance plans or access to discounted healthcare services for their members. While these options are less common than traditional employer plans, they can be worth investigating, particularly if you are part of a larger gig community in a specific industry. These plans might not offer premium tax credits, but they could provide competitive rates or specialized benefits.

4. Telehealth and Urgent Care

To manage day-to-day healthcare costs, gig workers can leverage telehealth services for routine consultations and minor ailments. Many insurance plans now cover telehealth, and it can be a convenient and cost-effective way to access medical advice without the higher costs of an emergency room visit. For non-life-threatening but urgent issues, urgent care centers are typically much more affordable than emergency rooms.

Future Outlook for Gig Worker Healthcare

The future of Gig Worker Healthcare 2026 and beyond remains a topic of ongoing discussion and potential legislative action. While the enhanced ACA subsidies are currently extended, their long-term permanence is subject to political will. Advocates for gig workers continue to push for more stable and comprehensive healthcare solutions, including portable benefits models that could allow gig workers to accrue benefits like health insurance, paid time off, and retirement savings across multiple platforms.

As the gig economy continues to expand, it’s increasingly likely that policymakers will need to address the unique needs of this workforce. Staying informed about legislative developments and advocating for policies that support affordable healthcare access will be crucial for gig workers. In the meantime, leveraging the existing frameworks, particularly the ACA’s premium tax credits, remains the most effective strategy for securing affordable health insurance.

Conclusion: Empowering Gig Workers with Affordable Healthcare in 2026

Access to affordable healthcare is a fundamental right, not a luxury, and for the millions of Americans thriving in the gig economy, it’s a critical component of financial stability and personal well-being. The enhanced premium tax credits available through the ACA, projected to continue into 2026, offer a significant opportunity for gig workers to secure comprehensive health insurance without undue financial strain.

By diligently estimating income, actively navigating the Health Insurance Marketplace, understanding the benefits of advance premium tax credits and cost-sharing reductions, and meticulously reconciling tax credits at year-end, gig workers can dramatically reduce their healthcare expenses. Furthermore, exploring options like Health Savings Accounts, Medicaid, and professional associations can provide additional layers of financial protection and access to care.

The journey to affordable Gig Worker Healthcare 2026 requires proactive engagement and informed decision-making. By taking the time to understand these mechanisms and utilizing the available resources, gig workers can not only protect their health but also solidify their financial foundation, ensuring that the flexibility and independence of the gig economy truly lead to a more secure future. Don’t let the complexities deter you; the benefits of affordable, quality health insurance are invaluable.